Successful real estate development is about leaving a lasting impact on future generations – creating unique spaces where people enjoy living, showing up to work, or spending their free time.

But even the most creative spaces never become a reality if the project is not also profitable – developers need to make money too. So, before a project is greenlit, it would be wise to conduct a feasibility study to evaluate its viability.

But here's the thing about the phrase "feasibility study." It's a term that has lost much of its meaning over the years – corporate middle managers have co-opted it as a means of sounding productive by throwing around buzzwords and jargon.

Can’t you picture Michael Scott asking for a feasibility study before stepping back into his office for another 4-hour block of “creative time?”

So, in this article, we will focus on defining a real estate development feasibility study, breaking it down into its parts, and covering what you need to know to assess the viability of your development.

What is a real estate development feasibility study?

Think SWOT analysis, but instead of vapid management consulting corporate speak, a quality development feasibility study dives into the strengths of weaknesses of a project within a specific market.

Before you outlay a bunch of capital pursuing a project, you'll want to ensure that it provides a certain profit level or exceeds certain financial feasibility thresholds.

A real estate development feasibility study is typically conducted as part of the project's initial due diligence.

It seeks to offer a roadmap for a potential project by assessing all site investigation, research, and preliminary due diligence items against potential problems and their financial implications.

The main purpose of a feasibility study is to provide a predictive analysis of the success of the overall project and the probability of various outcomes.

A feasibility study will also weigh competitor data, municipal-specific requirements, demographic trends, and macroeconomic implications - developers will have much more insight into a project's potential snafus.

The cost of mistakes during a development project

Mistakes during the real estate development process come in different shapes and sizes.

Some are avoidable – lack of experience and expertise or mismanagement and poor research can result in dealing with potentially foreseeable issues.

Other mistakes may be less apparent – political risk can be a huge question mark during a project, even for experienced developers.

In the early stages of a development project, enthusiasm is typically high, and that’s when a real estate developer is more prone to making silly mistakes.

Commonly, developers will overpay for land or buy the wrong type of property entirely – that could result from underestimating overall costs or just buying a property that doesn't meet the needs of a proposed project. Site selection mistakes frequently lead to project failure.

It’s also not uncommon to see developers overextend themselves during due diligence. If you fail to identify critical feasibility items early and fail to sequence your real estate due diligence activities properly, you leave yourself financially exposed.

Or even worse, what if you enter the wrong market entirely? Some developers build for personal taste – that rarely ever works out. Others fail to consider the market's needs or get swept into the craze over fads and flashy headlines.

The reality is that mistakes made during a development project can range from thousands of dollars to upwards of 7-figures.

But there is good news.

Conducting a feasibility study significantly mitigates project risks. It forces the developer to understand their target market, assess relevant political, land entitlement, and development unknowns, and ultimately determine the profitability of a project.

Components of a real estate development feasibility study

Market analysis

An in-depth market analysis is the core of any development feasibility study.

First and foremost, you’ll want to begin by charting historical data on the given market and submarket you're proposing to enter. Consider collecting data on the following critical rental metrics:

- Lease rates by property type and bedroom count (if you’re proposing a residential or multifamily project)

- Historical vacancy rates

- Average time to re-let space upon vacancy

- Property absorption statistics

- Local housing market activity

That data will give you a much better insight into the type of real estate development strategy that makes sense for your given market. Additionally, it's critical also to consider market-specific living and employment metrics like:

- Data on population in-migration growth

- Job growth and nearby employment centers

- Major employers and proposed future corporate relocations

- Workforce education levels

- Data on the number of nearby households and income levels

- Nearby amenities and access to major highways

- Walkability and quality of public transportation

Once you’ve identified and analyzed the key metrics for your given market, it's important to chart that data and extrapolate for future market trends. Historical data is an essential tool but only tells you part of the equation. A successful development project hinges on a market's continued growth and vibrancy for years to come.

But, you also need to ask yourself how these market forces impact your development strategy.

Based on the data you collected, what types of land development projects will most likely be successful? For example, if a given market has a robust entry-level employment feeder system, possibly by being colocated near a university, a well-positioned multifamily property may make sense. This is especially true if the area is already lacking in the supply of affordable starter homes.

Another factor to investigate is political risk. For example, if your proposed project isn't allowed "by-right" on a property or similar projects have faced resistance from the local planning department or city council, it’s worth considering.

And while political risk may not be quantifiable in terms of dollars and cents, it can lead to additional expenses for attorneys and more complex land entitlement procedures.

If there is a serious question about the possibility of a project not being approved, assigning a probability to that outcome is wise. Then you'll be able to develop several different profitable courses of action, during initial due diligence, in the event you need a contingency plan.

Competitive analysis

Think SWOT analysis from business 101 - a competitive analysis overviews the existing competitors and opportunities in a given market.

There is something to be said about having a first mover advantage. An innovative company may deliver a product or service and create a market for something we didn't even know we needed.

But that’s a risky process. And companies that move too early are frequently left flapping in the breeze.

You don't have to be an innovator to make money. Some of the most successful projects and companies are the ones that don't try to reinvent the wheel – they do something folks are already doing and do it a bit better.

So, a competitive analysis aims to understand what competitors have already developed property in your target market and evaluate their strategies to determine strengths and weaknesses relative to your own business.

Additionally, it is essential to consider where there may be supply or quality gaps in the marketplace – what consumer needs aren't being met?

After a development feasibility study competitive analysis, you should have insight into:

- The position of your competitors in a market

- An understanding of what is working and what isn’t for market competitors

- Any gaps in the market that need to be filled

- A concept for brand positioning as you enter the market

Ultimately, even a thorough competitive analysis won't ensure that your project will be successful. It will, however, highlight what has worked in the past and offer a framework from which you can make informed market entrance and development product placement decisions.

Real estate development model & financial analysis

The single most crucial feasibility metric for a new real estate development project is whether it's profitable or not.

Even the most selfless, mission-driven real estate developers are beholden to lenders' and outside equity partners' financing and underwriting standards. So, unless you're self-financing a deal, if the project isn’t profitable, you probably won’t be able to receive development financing.

The financial analysis determines a project's expected return on investment and the timing of cash flows over the project's life.

And one of the significant challenges to consider is that most developments don't see revenue until several years after a project begins. This is because, before lease-up and property stabilization, a large amount of capital is required for real estate due diligence and feasibility work, land entitlement, permitting, and construction.

So, you have cash out the door without the prospect of cash inflows for several years – that makes cash flow timing and financial projections even more critical to successfully analyzing a project.

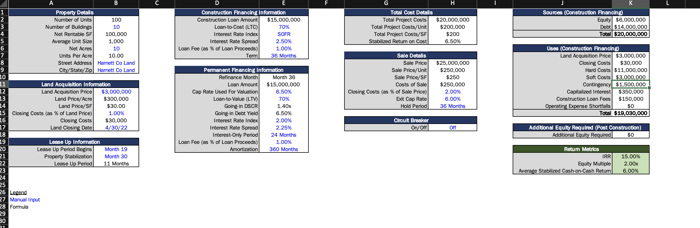

There are several critical components of a real estate development model you need to consider:

Land & site development costs

The term ‘development costs’ is frequently used as a catchall to describe all the costs associated with developing a site. But that can be misleading and often leads to poor assumptions.

For the sake of our development models, land and site development costs generally include: the cost of the land and an estimate of all sitework and land development costs, which consists of all earthwork, utilities, off-site improvements, etc.

Construction costs

Construction costs are generally broken down by hard costs vs. soft costs, which differentiate between whether or not the expenses are related to the physical construction of the building. From a cost control and a budgeting standpoint, it's important to distinguish between hard and soft construction costs as a part of your financial analysis.

Depending on the type of real estate development model you build, it's worth considering using an s-curve to forecast your construction and site development costs. An s-curve better matches the timing of construction cash outflows against the forecasted percentage of work completed at various stages throughout the process.

It's also important to incorporate a hard and soft cost contingency to guard against unexpected price fluctuations.

Revenue & sales assumptions

Depending on the type of project exit, a developer will either sell the project after construction or retain the project through lease-up and a predetermined hold period.

If the plan is to sell a property following completion, it will be important to incorporate comparable sales data into the model to anticipate revenue for selling the property after commissions.

If instead, the plan is to lease up and manage the property, you'll need to incorporate relevant rental statistics specific to the type of property you're bringing to market.

Critical to both exit scenarios are realistic and conservative property absorption and lease-up rates. For instance, how quickly do comparable properties sit vacant on the market? Or how long does it take to sell similar projects in the submarket?

These assumptions will ultimately offer insight into the anticipated carrying costs associated with the project and how long it will take a project to break even.

Expense assumptions

We've already discussed costs associated with the actual development and construction of the property. But if your plan is to hold the project, what about expenses related to the actual property management?

It’s critical to account for the property's operating expenses as part of your financial analysis. Consider expenses like:

- Taxes

- Insurance

- Repairs and maintenance

- Contract services

- Utilities

- CAPEX budget

- Property management

Additionally, you’ll want to associate an annual expense growth rate with these costs to account for inflation and other macroeconomic factors.

Financing assumptions

Modeling your financing package to fund a project can be a significant challenge. There are a variety of different ways to finance a development project.

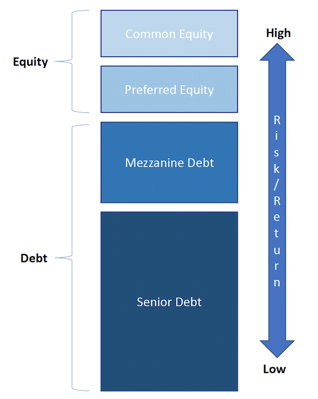

The capital stack can be comprised of different debt and equity financing types. Each financing source comes with an associated cost of capital that will impact the project's overall profitability.

First, you must address several critical assumptions as part of your financing package. For example, if incorporating some form of senior debt, you'll need to account for a loan-to-cost percentage and an interest rate assumption. If you're financing the project through some portion of limited partner equity, you'll need to account for the timing and size of any preferred returns and partner distributions.

These assumptions and any underlying financing costs and interest accrued during development and construction must be accounted for in your development model.

Tying everything together for your financial analysis

Once you’ve compiled all the data and assumptions into your development analysis, you’re ready to model your financial projections.

Most models rely on a discounted cash flow (DCF) analysis to determine critical financial metrics. Therefore, you'll first need to calculate the project's free cash flows.

A project’s free cash flows represent the project’s underlying cash flows after all revenue, expense, and financing assumptions have been accounted for.

Once you've quantified free cash flows for the project hold period, you can calculate critical financial metrics like net present value (NPV), internal rate of return (IRR), payback period, equity multiple, and cash-on-cash return.

Your real estate development model should also include a sensitivity analysis to account for fluctuations in critical assumptions like:

- Debt interest rate

- Revenue and expense assumptions

- Anticipated project exit capitalization (cap) rate

- Loan-to-cost ratio

This “what if” exercise will illuminate how sensitive your project’s profitability margin is to the worst- and best-case scenario.

Why are real estate development feasibility studies important?

Remember those costly mistakes we talked about earlier? You’ll want to avoid those. And a real estate development feasibility study is the most critical thing you can do to ensure you’ve done quality market research, accounted for potential obstacles, and set your project up for success.

Developing a property is much different than traditional buy-and-hold real estate strategies. Projects are more complex, the stakes are more significant, and the potential downside is often much greater.

All business endeavors pose some level of risk. But a feasibility study examines and quantifies that risk to determine if it’s worth taking and how profitable the project will be.

Feasibility studies are also used to pitch potential investors and lenders on the viability of a project.

Ultimately, projects backed by informed research and data have a much higher likelihood of success.

A real estate consultant can help craft your development feasibility study

Are you thinking about pursuing a development project? Consider leveraging the expertise of a real estate development consultant as you investigate feasibility before it’s too late.

A feasibility study is a fundamental step in the due diligence process. Not only to serve as a business plan of sorts for you but also as a tool to help onboard potential capital partners.

To equate it with risk management – a real estate consultant can direct your efforts in investigating all critical feasibility items and codifying those findings into a roadmap to guide your project - even if you're unsure where to start.

And Marsh & Partners can help - ultimately delivering you maximum project value and reducing project risk.

You can learn more about our real estate consulting services here for more information on how we can add value to your next project.